Blue World Employment Situation Report Analysis

Release Date: Usually on the first Friday of the month

Release Site: www.bls.gov

Market Impact: Usually Very High

Management Value: Critical

Date: Friday, April 06, 2018

Brain Surgery is not Rocket Science to a Brain Surgeon©

Cooling was expected but this was kinda weird. Once we look at all the net-nets it was a mixed report with an unmistakable positive lean even though the headline shows a substantial miss. Getting deep in the weeds and doing a lot more math than usual was key to understanding what this one really said. There are, of course, already thousands of “expert” “analyses” out there by both sides of the political aisle and financial industry with their own slants, so as always, read those for amusement and stay here for the actionable intelligence needed for strategic management decision making!

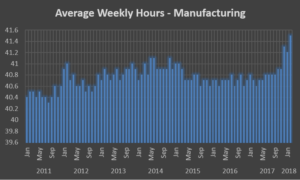

At the headline we see 103k whereas most consensus estimates called for 175k to 200k. The good news is that of the 103k, 102k were Private Sector adds which also picked up a positive revision from last month pushing the YTD 2018 average over 200k. Most of the positive developments from our go-to stats in last month’s monster report held up and wages hinted at some pressure. The work week length was steady and Manufacturing was a big winner again. The Diffusion Indexes returned from outer space but remained comfortably (and more sustainably) above 60. The table above shows annual averages back to 2014 for some of those key stats and you can see which are stubborn and which are making progress.

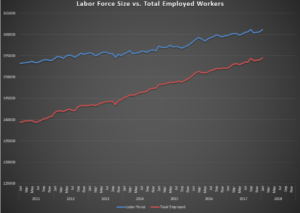

Concerns? A few. Retail got beaten up and that is consistent with yesterday’s Challenger layoffs report. Participation Rate and Not in Labor Force numbers continue to disappoint and there were too many Part-Time jobs but that tends to be volatile. We don’t think that this will force the hawks from their perch at the Fed so hopefully they’ll leave rates alone a while longer but they seem to look for any excuse these days.

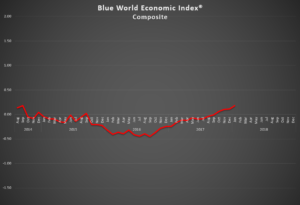

Overall it was a good March for the economy. The Blue World Economic Index® made a nice move led by Employment and Manufacturing. Services looked good with rare and welcome tri-confirmation of strength despite slight pullbacks in ISM and PMI’s non-manufacturing reports.

From our consulting point of view the light is either Red or Yellow. We’ve never seen a pure Green light but we have perceived some blue tint coming in of late so there may be some Green out there…but we’ll never admit it!

Have a great April and we’ll see you back here in May.

Thanks for reading, and please stay tuned…

Release Site: www.bls.gov

Every effort is made to ensure accuracy of data transcription but accuracy cannot be guaranteed. The official release site should be cross referenced. The analysis represents the opinion of Blue World Asset Managers, LTD. who does not warrant or guarantee predictions based on its analysis.

©Blue World Asset Managers, LTD Friday, April 06, 2018