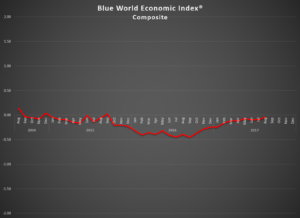

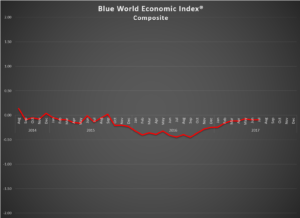

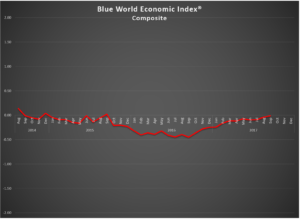

Blue World Economic Index®

Scale: -2 to +2

Release Date: Usually the Last or First Business Day of Each Month

Release Site: www.blueworldassetmanagers.com

Management Value: Critical

Date October 3, 2017

Analysis

The economy’s flirtation with a positive reading is as tantalizing as a butter-seared, blood-rare Porterhouse, wild rice and a snifter of cognac is to me on a Saturday night! TMI? Apologies.

The Blue World Economic Index® made a solid move from -.4 to -.1 for the month of September 2017. It must be noted that looking at a lot of the reports would suggest bigger changes from last month in either direction, but we exercised a bit more restraint due to the awareness of the continued but temporary impact of the active hurricane season. There was also a material impact from short and long-term trend upgrades in GDP from -1 to -.5 because the trends are weighted more heavily than the current month’s report.

That said, we expected worse from the hurricanes, especially in reports that post in the second half of the month, and the consumer appears to have already gotten over it. Below we’ll talk about weakness in Real Estate, but there is a lot of thinking out there that the weakness represents a short-term rebalancing and may be a harbinger of better things to come later next year. The Chicago Fed has been the only contrarian in the Fed sub-group two months in a row, which is a bit perplexing and concerning since that report is uniquely national in scope rather than regional like the others we follow for that group, and the regionals are knocking the cover off the ball.

December Fed meeting, you ask? The late entries of Personal Income and Outlays, Farm Prices, and GDP Inflation coupled with the mid-month reports of Producer Price Index-Final Demand and the Consumer Price Index all suggest inflation still resides in the where-are-they-now-file, but there are, as we’ve said, some other positives. We think there are arguments for the doves and hawks, but we are taking the under this month and saying we’ve seen the last of the hikes for 2017.

The Numbers

Of the eight major categories, five are still above water. They are Consumer, General, Manufacturing, Real Estate, and Retail. Of those, all but one, Real Estate, posted gains since last month, but recall some of the conflicting signals in Retail where negative scores for Motor Vehicle Sales and Retail Sales were cancelled out by equal and opposite scores in Business Inventories and E-Retail, leaving the notoriously contrarian Red Book report to carry the ball. Manufacturing continues to excite with the Fed AND non-Fed groups advancing .03. Employment and Inflation are still underwater, where Employment slipped fractionally, but Inflation, while improved .11, is still solidly negative at -.37. Services remained unchanged at -.16.

We’ll see what else the hurricanes have to offer the fourth quarter, and with high stakes policy issues like tax reform coming up we see volatility and excitement from street level to Wall Street on tap!

The Blue World Jobs Report Analysis will post on Friday. Have a great October, a wonderful Halloween and we’ll see you back here at the opening of November.